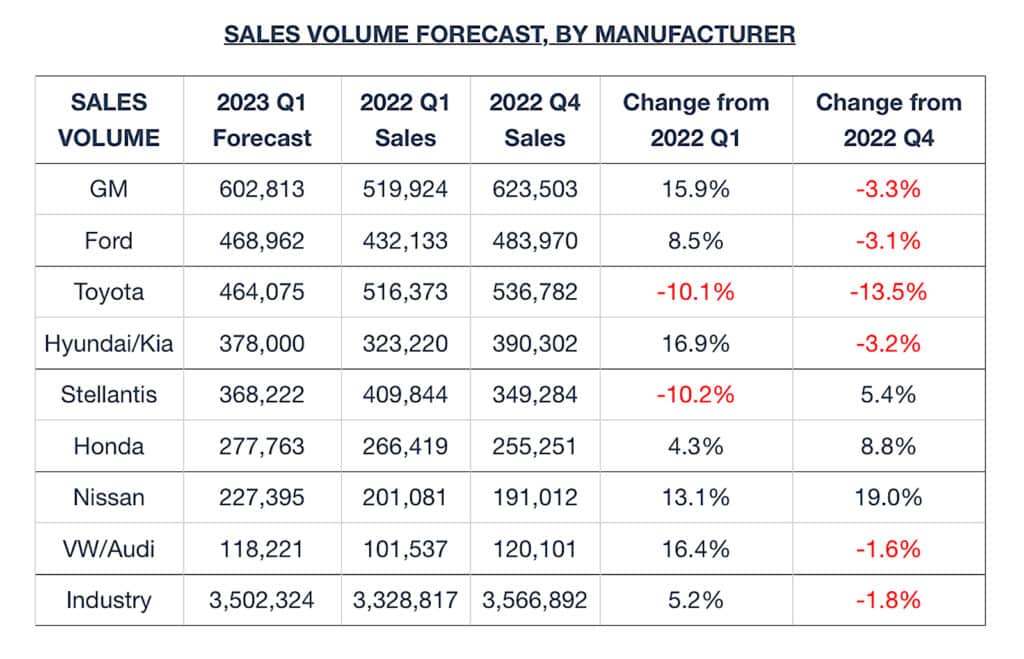

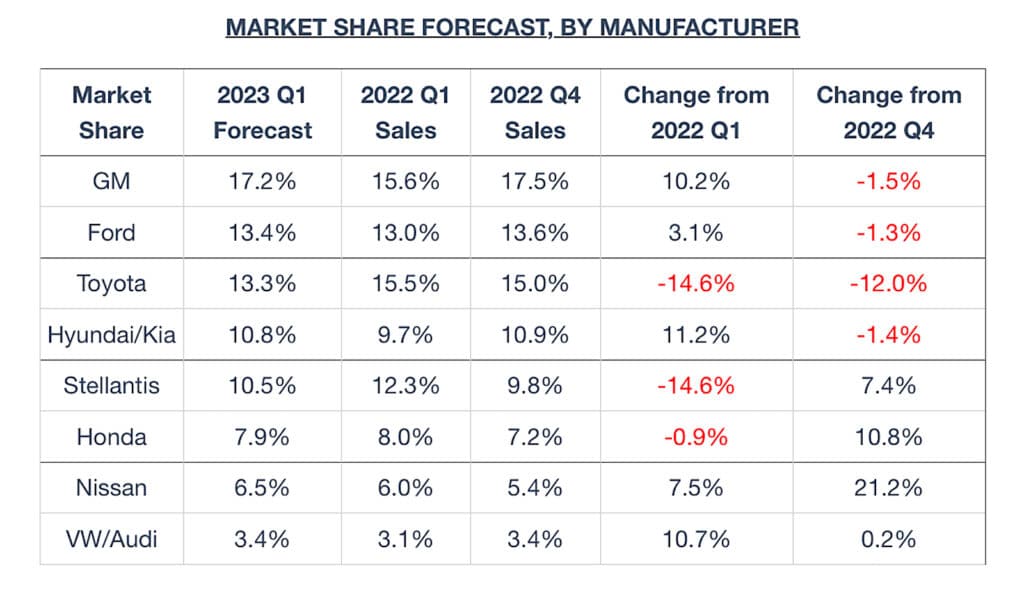

Automakers are expected to sell more new vehicles in the first quarter of 2023 than they did during the same period last year, with the total rising 5.2% to 3.5 million cars, trucks and SUVs.

However, that number is down from the fourth quarter last year by 1.8%. That drop is an indicator that changes in the industry are moving sales to a more normal pace, according to analysts at car shopping experts Edmunds.com.

A joint forecast issued by J.D. Power and LMC Automotive projects that new-vehicle sales for the month of March will reach 1,330,700 vehicles. The figure, which includes both retail and non-retail sales, represents a 6.2% increase over the same month last year. Power and LMC echoed Edmunds forecast of 3.5 million new vehicles sold in Q1.

During the past several months, inventory levels have risen. This gives buyers more options and, perhaps more importantly, more time to decide what they want to buy. That’s reflected in the average number of days it takes for a dealer to sell a vehicle once it hits their lot, moving from 24 days in Q1 2022 to 34 days in Q1 2023.

“The auto industry’s wild rollercoaster ride the past few years has finally begun the transition to a smoother, more predictable one as inventory continued to improve in the first quarter,” said Jessica Caldwell, Edmunds’ executive director of insights.

“Although the market is nowhere close to the bargain-heavy landscape that consumers came to expect prior to the pandemic, car shoppers should be happy to see that some incentives are cropping up after more than a yearlong drought as inventory levels continue to rise.”

Changing buyer landscape

Analysts agree there is still pent-up demand from new vehicles, but it’s slowly abating and as the days needed to sell a vehicle continues to rise, new vehicle buyers are going to need to adjust their plan of attack when buying a vehicle. They are beginning to enter an environment that may be tilting in their favor — slightly.

“Consumers planning on making a car purchase will still need to do their research and prepare to make a move if they find a vehicle that they like, but they can at least take a breath and not feel as pressured to jump at every piece of inventory the minute it hits the market,” said Ivan Drury, Edmunds’ director of insights.

With slowing demand and higher supply, average transaction prices — which are now approaching $50,000 for an average new vehicle — may begin to come down, especially if or when automakers begin to bolster incentives again.

“For current car owners who have been waiting for the market to cool before getting into a new vehicle, now is the time to begin paying close attention to trade-in values, which are continuing to soften as new car inventory grows. If you time things just right, you might be able to maximize your trade-in value and score a new car with a bit of a discount,” Drury said.

Although used car prices have been declining for several months, their values are still strong. Edmunds noted the average age of trade-in vehicles was higher in the first quarter of this year, 5.9 years, versus the same period last year, 5.3 years. So the playing field is fairly level as everyone’s vehicles are moving in the same direction, in terms of value.

Potential headwind

A big factor influencing the decision to buy is the rising interest rates. The Federal Reserve raised them again just a week ago by a quarter point. The rate hike, the ninth consecutive one, reflects ongoing concern by the organization about inflation, which continues to drop. It was 6% in February after coming in 6.4% in January. It was 9% last summer.

That said, interest rates on new vehicles are now at about 6.5% on a four-year loan after being in the 4% range just about year ago, according to Statista.com.